Increasing the Massachusetts RPS: It Makes Economic Sense

In 2016, a small group of energy wonks and climate activists attempted to reconcile Massachusetts legislative energy proposals with the state’s mandated Global Warming Solutions Act (GWSA) targets and the larger, national emission reductions needed to keep warming to 1.5°C or 2°C. This group quickly came to the conclusion that Massachusetts policy proposals were inadequate.

We knew the Renewable Portfolio Standard (RPS) proposals at the time—a 2% increase was considered aggressive—were lacking, but wanted to model the impacts of a large annual RPS increase (i.e. 3% or more) before advocating for it. We wanted to be able to answer the following questions:

- Is it feasible within the existing power market structure?

- How will it impact utility ratepayers?

- What effect will it have on jobs?

We now have our answers. Thanks to modeling performed by Synapse Energy & Sustainable Energy Advantage, we know that aggressively increasing the Massachusetts RPS is not only feasible, but will have a minimal impact on utility bills and a large positive impact on jobs. These organizations modeled the energy, climate and economic effects of various RPS and natural gas price scenarios, ranging from status quo (1% annual Massachusetts increase) to increasing the MA RPS by 3% each year along with a 1.5% increase to Connecticut’s RPS (roughly equivalent to increasing the MA RPS by 3.75% alone).

The analysis revealed that there are no economic barriers to increasing the RPS. Any barriers remaining are purely political.

Utility bill impacts

Modeling of different RPS scenarios revealed only modest electricity bill increases for residential customers. The most aggressive scenario modeled (3% MA RPS with 1.5% for CT) resulted in an average monthly bill increase of only $2.17 between 2018 and 2030. Although the modeling focused on residential costs, the authors of the study expect that industrial and commercial customers “would see similarly small bill impacts to those described for residential customers.”

How does a Massachusetts RPS increase affect prices specifically?

As the RPS increases, we see a lowering of wholesale market prices. Renewable energy systems displace higher-cost generators when renewable systems are able to produce electricity. This leads to greater utilization of low-cost resources and lower average wholesale prices.

Modeling revealed no significant impact on capacity prices (the price paid to generators to maintain future dispatchable electricity capacity) through 2030 even with an annual MA RPS increase of 3%.

The modest utility bill increases we see in the 3% MA RPS scenario come from the cost of purchasing RECs (which will increase in price with increased demand) along with additional transmission and distribution costs associated with higher levels of renewable generation. These costs are partially offset by the reduction in wholesale prices, but the net result is a small increase in average monthly electricity bills.

Protection from rising natural gas prices

Increasing the RPS can protect Massachusetts residents from future volatility in natural gas prices. Massachusetts has become overreliant on natural gas, which is the primary driver of the price we pay for electricity. According to the Energy Information Administration (EIA), 66% of our electricity was generated by natural gas in 2016. Modeling shows that if gas prices rise significantly as some expect, increasing the RPS substantially could save New England consumers up to $2.1 billion in wholesale costs between 2018 and 2030.

Per the EIA, natural gas prices are likely to rise due to production expansion into more expensive areas combined with increases in liquefied natural gas (LNG) and petrochemical exports. These exports will decrease the domestic supply of natural gas, forcing prices upward. Trump administration actions may also increase demand. These include withdrawal from the Paris Climate Accord, promoting pipeline expansion efforts that increase exports, and removing regulatory barriers to LNG exports.

Natural gas prices will almost certainly rise in the future, but an aggressive shift to renewable energy can minimize the effect on electricity prices.

Impact on jobs

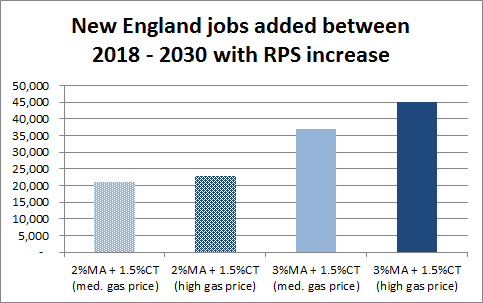

Modeling of a 3% MA RPS reveals a net positive impact on jobs, with higher RPS increases resulting in more jobs in the region. In the years between 2018 and 2030, we find a net increase (accounting for job losses in the fossil fuel industry) of 18,000 jobs from a 2% MA RPS increase combined with a 1.5% increase in CT, and 33,400 jobs with a 3% MA increase combined with a 1.5% CT increase. A more aggressive RPS means more jobs.

Net job gains from various RPS increase and natural gas price scenarios

Net job gains from various RPS increase and natural gas price scenarios

We also find from the analysis that maintaining the current 1% annual MA RPS increase or even moving to a 2% increase without a change to the Connecticut RPS will not boost jobs. The required procurement of 1,600 megawatts of offshore wind in the 2016 Energy Diversity Act will shift the market, resulting in the supply of renewable energy (as measured in RECs) outpacing demand. The RPS is meant to drive renewable energy development, but the Massachusetts RPS will simply perform backfill duties unless it’s strengthened.

Summary

Massachusetts has done an admirable job of promoting renewable energy growth, yet we are still behind in meeting our climate climate goals. Wind procurement mandates in the Energy Diversity Act will help, but a significant RPS increase is needed to further promote renewable energy growth in the state and region. All of our electricity must be generated from carbon-free sources in the not-too-distant future if we have any hope of limiting warming to 1.5C or 2C.

Fortunately, we have evidence that significantly increasing the RPS will provide two critical economic benefits with minimal cost to ratepayers:

Risk reduction/price stabilization: a large RPS can protect electricity ratepayers from rising natural gas prices and help stabilize volatile electricity rates associated with our dependence on natural gas. The wind and sun are free, while natural gas prices fluctuate with supply, demand, politics and policy.

Jobs: increasing the RPS will result in a net increase in regional jobs, with more jobs associated with greater rates of RPS growth.

Massachusetts can hedge against the risk of rising natural gas prices, reduce emissions and create jobs by aggressively increasing the RPS—all with little cost to ratepayers. This is a policy decision that’s good for business, good for citizens and good for the state.

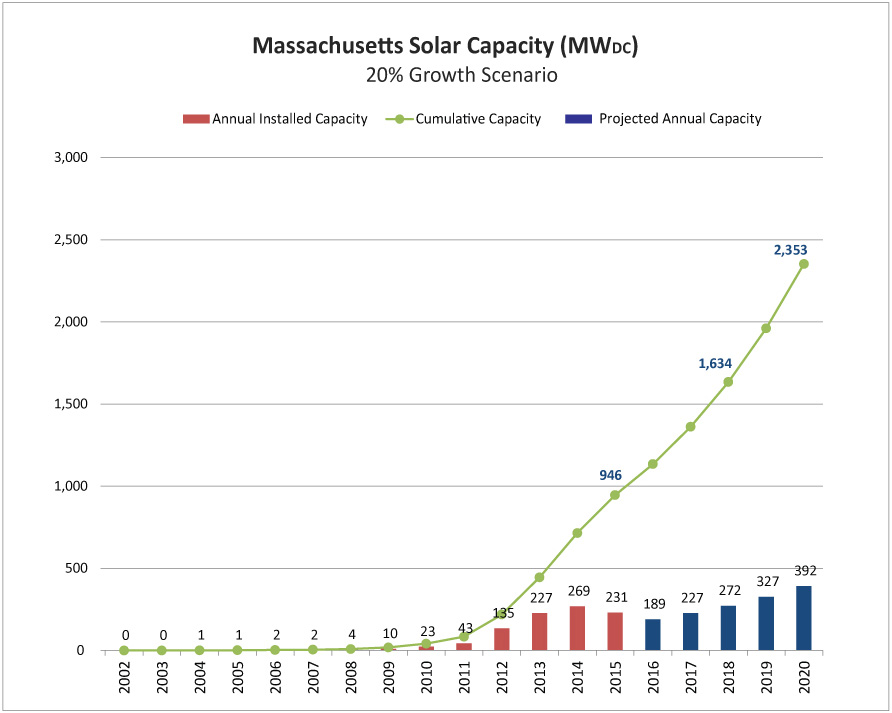

Massachusetts Solar capacity projections assuming 20% annual growth from 2016 to 2020.

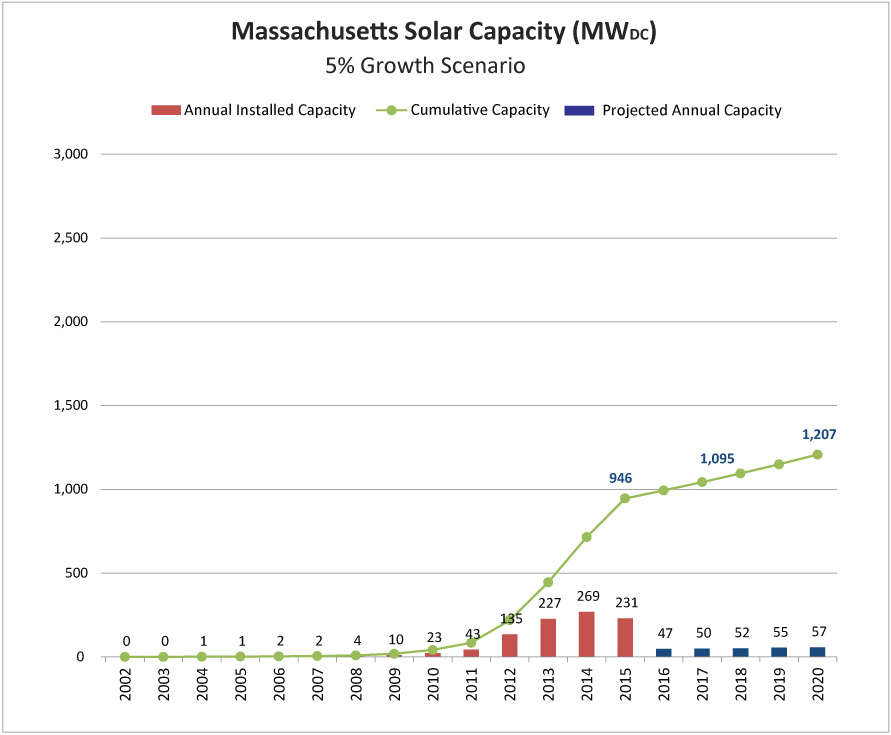

Massachusetts Solar capacity projections assuming 20% annual growth from 2016 to 2020. The “Nevada” Scenario: Massachusetts solar capacity projections assuming 5% annual growth from 2016.

The “Nevada” Scenario: Massachusetts solar capacity projections assuming 5% annual growth from 2016.